Audit Committee Terms of Reference

Audit Committee

Terms of reference

(Approved by the committee on 21 October 2025

Ratified by the Board of Directors on 29 January 2026)

1. Name of Committee

The name of this Committee is the Audit Committee

2. Composition of the Committee

The members of the Committee and those who are required to attend are shown below together with their role in the operation of the Committee.

Members

| Title | Role in the Committee |

| Non-executive Director (Chair of the Committee) | Committee Chair and responsible for evaluating the assurance given and identifying if further consideration / action is needed.

Non-executive Directors provide constructive challenge and strategic guidance, and lead in holding the executive to account. In particular, Non-executive Directors should scrutinise the performance of the executive management in meeting agreed goals and objectives, receive adequate information and monitor the reporting of performance. They should satisfy themselves as to the integrity of clinical and other information, and make sure that clinical quality controls, and systems of risk management and governance, are robust and implemented. (Code of Governance for NHS Provider Trusts, NHS England 2022) |

| 2 Non-executive Directors | Responsible for evaluating the assurance given and identifying if further consideration / action is needed.

Non-executive Directors provide constructive challenge and strategic guidance, and lead in holding the executive to account. In particular, Non-executive Directors should scrutinise the performance of the executive management in meeting agreed goals and objectives, receive adequate information and monitor the reporting of performance. They should satisfy themselves as to the integrity of clinical and other information, and make sure that clinical quality controls, and systems of risk management and governance, are robust and implemented. (Code of Governance for NHS Provider Trusts, NHS England 2022) |

While specified Non-executive Directors will be regular members of the Audit Committee, any other Non-executive Director can attend the meeting on an ad-hoc basis if they wish and will be recognised as a member for that particular meeting and if necessary will count towards the quoracy.

Attendees

| Title | Role in the group / committee | Attendance guide |

| Chief Financial Officer | Key responsibilities regarding audit and reporting | Every meeting |

| Internal Audit representation | Independent assurance providers | Every meeting |

| External Audit representation | Independent assurance providers | Every meeting |

| Local Counter Fraud representation | Independent assurance providers | Dependant on the agenda |

| Associate Director for Corporate Governance | Committee support and advice | Every meeting |

The Chair of the Audit Committee shall be seen as independent and therefore must not Chair any other governance committee either of the Board of Directors or wider within the Trust.

Executive Directors and other members of staff may attend by invitation in order to present or support the presentation of agenda items / papers to the Committee. Executive Directors will be invited to attend a meeting where a low assurance and/or limited assurance report has been issued by Internal Audit and is on the agenda to be discussed.

The Chair of the Trust and the Chief Executive will be invited to attend the Audit Committee once per year.

2.1 Governor Observers

The role of the Governor at Board Sub-committee meetings is to observe the work of the Committee, rather than to be part of its work as they are not part of the formal membership of the Committee. The Governor observes Board Sub-committee meetings in order to get a better understanding of the work of the Trust and to observe Non-executive Directors appropriately challenging the Executive Directors for the operational performance of the Trust.

At the meeting the Governor observer will be required to declare any interest they may have in respect of any of the items to be discussed (even-though they are not formally part for the discussion). Governors will receive an information pack prior to the meeting. This will consist of the agenda, the minutes of the previous meeting and summaries of the business to be discussed. Governor observers will be invited to the meeting by the Corporate Governance Team. The Chair of the meeting should ensure that there is an opportunity for Governor observers to raise any points of clarification at the end of the meeting.

2.2 Associate Non-executive Directors

Associate Non-executive Directors (ANEDs) will be invited to attend Board Sub-committee meetings as part of their induction. They will attend the meeting in the capacity of observer only, unless invited to contribute by the Chair in circumstances that support the ANEDs development and understanding. This is so the accountability of the substantive members of the Committee is maintained.

ANEDs will be invited to meetings by the Corporate Governance Team and will be sent copies of the meeting papers.

3. Quoracy

Number: The minimum number of members for a meeting to be quorate is 2. Attendees do not count towards this number.

Deputies: Non-executive Directors do not have deputies. Non-core Non-executive Directors may be asked to attend if there is a risk to the meeting not being quorate.

Attendees should nominate a deputy to attend in their absence. A schedule of deputies, attached at appendix 1, this should be reviewed at least annually to ensure adequate cover exists.

Non-quorate meeting: Non-quorate meetings may go forward unless the Chair decides otherwise. Any decisions made by the non-quorate meeting must be reviewed at the next quorate meeting.

Alternate chair: If the Chair of the Audit Committee is not available the meeting shall be chaired by one of the other Non-executive Directors.

4. Meetings of the Committee

Meetings may be held face-to-face or remotely as is considered appropriate. Remote meetings may involve the use of the telephone and / or electronic conference facilities.

Frequency: The Audit Committee will normally meet as required but will in any case meet no fewer than four times per year.

Urgent meeting: Any of the Committee members may, in writing to the Chair, request an urgent meeting. The Chair will normally agree to call an urgent meeting to discuss the specific matter unless the opportunity exists to discuss the matter in a more expedient manner (for example at a Board meeting).

Minutes:Draft minutes will be sent to the Chair for review and approval within seven working days of the meeting.

Papers: Papers for the meeting will be distributed electronically by the Corporate Governance Team five working days prior to the meeting. Papers received after this date will only be included if decided upon by the Chair.

Private Sessions of the Committee

At least once a year the Committee will meet privately with representatives from internal audit and external audit.

At the discretion of the Chair of the Committee, it may also choose to meet privately with the Chief Financial Officer and any other key senior officer in the Trust as may be required.

Members of the Committee will also meet together in private at a frequency determined by the Chair.

5. Authority

Establishment: In accordance with the NHS Act 2006 and the Code of Governance the Board of Directors is required to establish an Audit Committee as one of its Sub-committees.

Powers: The Committee is a Non-executive Committee of the Board of Directors and has no executive powers. The Committee is authorised by the Board of Directors to seek assurance on any activity. It is authorised to seek any information or reports it requires from any employee, function, group, or committee; and all employees are directed to co-operate with any request made by the Committee.

The Committee is authorised by the Board of Directors to obtain outside legal or other independent professional advice and to secure the attendance of persons outside the Trust with relevant experience and expertise if it considers this necessary.

Cessation: The Audit Committee is a standing Committee in that its responsibilities and purpose are not time limited. While the functions of the Audit Committee are required by statute the exact format may be changed as a result of its annual review of its effectiveness.

In addition, the Trust should periodically review its governance structure for continuing effectiveness and as a result of such a review the Board may seek to alter the format or the number of Non-executive Director core members of the Audit Committee.

6. Role of the Committee

6.1 Purpose of the Committee

The purpose of the Audit Committee is to provide the Board of Directors with assurance that:

- Clinical, financial reporting, compliance, risk management, and internal control principles and standards are being appropriately applied and are effective, reliable, and robust

- An effective governance framework is in place for monitoring and continually improving the quality of health care provided to service users to enable the Trust’s strategic objectives to be achieved.

| Objective | How the committee will meet this objective |

| We deliver great care that is high quality and improves lives | The Audit Committee has a core responsibility to scrutinise the Trust’s governance arrangements to determine that these are operating effectively and that the Trust is able to provide high quality care through these arrangements. |

| We use our resources to deliver effective sustainable care | The Audit Committee exercises scrutiny of the annual financial reporting of the organisation; on-going financial health; and controls designed to deliver efficiency, effectiveness, and economy for all Trust functions |

6.2 Guiding principles for members (and attendees) when carrying out the duties of the Committee

In carrying out their duties, members of the Committee and any attendees of the Committee must ensure that they act in accordance with the values of the Trust, which are:

- We have integrity

- We are caring

- We keep it simple.

6.3 Duties of the Committee

Notwithstanding any area of business on which the Committee wishes to receive assurance the following shall be those items on which the Committee shall receive assurance:

Board Assurance Framework

- Be assured that the organisation has in place an effective Board Assurance Framework

- Be presented with the Board Assurance Framework and receive assurance that this presents the up-to-date position in respect of controls, assurances and that gaps are being addressed, and be assured as to the completeness of the information included in the Framework

- Use the Board Assurance Framework to inform the Committee’s forward work plan, in particular focussing on those gaps that pose a major risk to the organisation.

Quality Account

- Be assured in respect of the process for delivering the Quality Account with the submission of a paper which explains how the Quality Account has been populated.

Risk Management

- Receive assurance as to the Risk Management Process (including structures processes and responsibilities for managing key risks), including the process for capturing and reviewing high and extreme risks

- Carry out the duties of Safety and Risk Champion.

Health and Safety

- Receive an annual report and regular update reports on health and safety management within the Trust

- Have oversight quarterly of the progress against the Health and Safety action plan

- Carry out the duties of the Health and Safety Champion.

Compliance and Disclosure Statements

- Be assured of the action taken by officers who have operated outside of the tender and quotation procedures

- Be presented with notification of any waivers of the Standing Financial Instructions and Standing Orders (for the Board of Directors and Board of Governors) and be assured of their appropriateness.

Annual Accounts and Annual Report

- Be presented with and review the main items / contentious items in the Annual Accounts, taking advice from the Chief Accounting Officer and the External Auditors as to accuracy, prior to advising the Board if the Accounts can be adopted

- Be presented with the ISA260 Report on the Annual Accounts and be assured as to the findings and the management actions agreed, also be assured that either there were no (or otherwise) significant findings

- Be presented with a periodic report setting out the progress against the recommendations made in the ISA 260 reports (pertaining to the last set of annual accounts) and be assured as to progress against recommendations / action plans.

Annual Governance Statement and Head of Internal Audit Opinion

- Be presented with the draft Annual Governance Statement and have an opportunity to input to the content

- Be presented with the final version of the Annual Governance Statement and be assured that it provides an accurate picture of the processes of internal control within the organisation

- Be presented with the Head of Internal Audit Opinion and be assured that this is an accurate assessment of the Trust and also be assured that the opinion is in accordance with the Annual Governance Statement.

Registers

- Be presented with the Losses and Special Payments Report to be assured as to the appropriateness of payments made and that control weaknesses have been addressed

- Be presented with the Sponsorship Register to be assured that it is complete, and that sponsorship received by the organisation / individuals is appropriate and has been applied for according to the procedure

- Be presented with the Hospitality Register to be assured that it is complete, and that hospitality received by individuals is appropriate, proportionate, and unable to be considered an inducement and has been recorded according to the procedure

- Be presented with the register of Management Consultants to be assured that it is complete and that consultants have been appointed appropriately, and according to the procedure.

Internal Audit

- The Committee shall ensure there is an effective Internal Audit function established by management that meets mandatory Global Internal Audit Standards and provides appropriate independent assurance to the Audit Committee, Chief Executive and Board of Directors. This will be achieved by:

- Consideration of the provision of the Internal Audit service, the cost of the audit function and (where the service is provided in-house) any questions of resignation and dismissal

- Review and approval of the Internal Audit strategy, operational plan, and more detailed programme of work, ensuring that this is consistent with the audit needs of the organisation

- Consideration of the major findings of Internal Audit work (and management’s response), and ensure co-ordination between the Internal and External Auditors to optimise audit resources

- Ensuring that the Internal Audit function is adequately resourced and has appropriate standing with the organisation.

External Audit

- The Committee shall review the work and findings of the External Auditor. In addition to this the Committee will:

- Make recommendations to the Council of Governors as to the appointment, reappointment, termination of appointment and fees of the External Auditor, and if the Council of Governors rejects the Audit Committee’s recommendations, it will prepare an appropriate statement for the Board of Directors to be included in the Trust’s Annual Report

- Review the audit program of work and fees and discuss with the External Auditor, before audit work commences, the nature and scope thereof

- Review External Audit reports together with the management response, and the annual governance report (or equivalent)

- Consider whether it is appropriate and beneficial to the Trust for the External Auditor to undertake investigative and advisory work for the Trust.

Counter Fraud

- Every NHS organisation is required by the NHS standard contract to have a counter fraud function. The counter fraud function’s role and responsibilities are based on the “Government functional standard 013: counter fraud (counter fraud standard)” and its interpretation for the NHS, “the NHS requirements”, which are defined and supported by the NHS Counter Fraud Authority (NHSCFA).

- The Committee shall satisfy itself that the organisation has adequate arrangements in place for counter fraud, bribery, and corruption that meet the NHSCFA’s standards and shall review the outcomes of work in these areas.

- With regards to the Local Counter Fraud Specialist it will:

- Review, approve, and monitor counter fraud work plans

- Receive regular updates on counter fraud activity

- Monitor the implementation of action plans

- Discuss NHSCFA quality assessment reports

- Receive a copy of the counter fraud functional standard return for awareness and to be reassured that the submission is consistent with the counter fraud progress updates presented to the Committee throughout the year

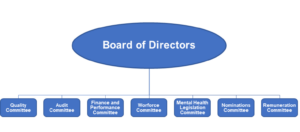

7. Relationship with other groups and committees

The Audit Committee is the primary governance committee providing an overarching governance role, having a direct relationship with other Board Sub-committees.

The Board Sub-committees will provide one of the main sources of assurance to the Audit Committee. However, this assurance will be validated by the work of, and reports from other sources of assurance including, but not exclusively, Internal Audit, External Audit, and Counter Fraud Services.

The following is a diagram setting out the governance structure in respect of assurance

The Committee has a duty to work with other Board Sub-committees to ensure matters are not duplicated.

8. Duties of the Chairperson

The Chair of the Committee shall be responsible for:

- Agreeing the agenda

- Directing the meeting ensuring it operates in accordance with the Trust’s values

- Giving direction to the minute taker

- Ensuring everyone at the meeting has a reasonable chance to contribute to the discussion

- Ensuring discussions are productive, and when they are not productive they are efficiently brought to a conclusion

- Deciding when it is beneficial to vote on a motion or decision

- Checking the minutes

- Ensuring sufficient information is presented to the Board in respect of the work of the Committee

- Ensuring the Chair’s report is submitted to the Board as soon as possible.

- Ensuring that governor observers are offered an opportunity at the end of the meeting to raise any points of

In the event of there being a dispute between any ‘groups’ in the hierarchy (in the case of this Board sub-committee, this would be between the Board and the Audit Committee and, in recognition of the nature of matrix working between the work of all Board sub-committees, the Audit Committee and any other Board sub-committee) it will be for the Chairs of those groups to ensure there is an agreed process for resolution; that the dispute is reported back to the ‘groups’ concerned; and that when a resolution is proposed the outcome is also reported back to the ‘groups’ concerned for agreement.

9. Review of the Terms of Reference and Effectiveness

The Terms of Reference shall be reviewed by the Committee at least annually and then presented to the Board of Directors for ratification, where there has been a change.

In addition to this the Chair must ensure the Committee carries out an annual assessment of how effectively it is carrying out its duties and make a report to the Board of Directors including any recommendations for improvement, along with any remedial action to address weaknesses. The Chair will also be responsible for ensuring that the actions to address any areas of weakness are completed.

Appendix 1a – Schedule of deputies

It may not be necessary or appropriate for all members (or attendees) to have a deputy attend in their absence. If this is the case please state below “no deputy required”.

| Full member (by job title) | Deputy (by job title) |

| Non-executive Director (Chair of the Committee). | Either one of the Non-executive Directors. |

| Attendee (by job title) | Deputy (by job title) |

| Chief Financial Officer | Deputy Director of Finance |

| Associate Director for Corporate Governance | Head of Corporate Governance |